Definition

Correlation Coefficient

The correlation coefficient between two real-valued random variables is defined as:

It is bounded, i.e.:

and it holds that:

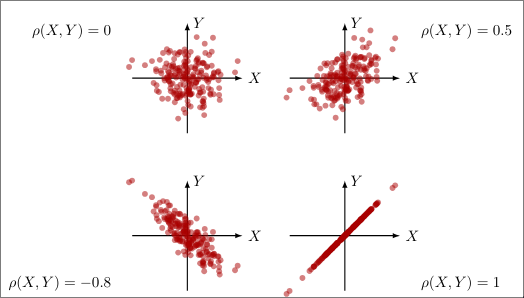

It measures the strength and direction of linear relationship between two quantitative variables.

Covariance

The correlation coefficient is the covariance of , scaled to variance 1 or standardised:

Examples